Libor ends in 2021 – Have you considered the impact on your transfer pricing?

HLB Thailand Transfer Pricing Team

In determining interest rates for various debt instruments, including inter-company financing transactions, the most widely used interest rate benchmark has been the London Inter-bank Offered Rate (LIBOR). LIBOR is a term-based rate, available in different maturity periods overnight, weekly, one month, three months, six months, 12 months, etc.

LIBOR will be phased out by the end of 2021 due to the following reasons:

- Measures an estimated interest rate instead of the actual interest rate; and

- An alleged bubble burst in 2012, several leading financial institutions (including Deutsche Bank, Barclays, Citigroup, JPMorgan Chase, and the RBS) were caught manipulating the LIBOR rate using inaccurate estimates of their borrowing costs to fix the LIBOR rates.

This raised questions over the validity and reliability of applying LIBOR as a reliable benchmark for financial/financing transactions. Therefore, regulators and market participants are preparing to transition away from LIBOR in existing and future arrangements.

LIBOR is often used in inter-company financing transactions, and the change will impact the financial sector as a whole in the following ways:

- Selecting a base rate that is accepted globally; and

- Whether the change will benefit companies in their current structures and planning (including hedging).

There is currently uncertainty around how multinational organisations will address the transition or how the arm’s-length margin/spread will be calculated.

New transfer pricing (TP) legislation has been in effect in Thailand since 2019, introducing mandatory TP documentation requirements and filing TP disclosure forms by certain taxpayers. TP regulations and guidance notes continue to be developed, with those issued to date aligning with the OECD’s TP guidelines.

The Thai Revenue Department has yet to provide any specific TP guidance on benchmarking interest rates. However, as Thailand largely follows the OECD, we anticipate the level of information required by the Thai Revenue Department would be as stringent as mentioned in the OECD’s TP guidelines. Read more: introduction to Transfer Pricing in Thailand.

Use of LIBOR in Thailand

In Thailand, US dollar LIBOR is used to calculate Thai Baht Interest Rate Fixing (THBFIX), used in financial transactions, in cash and derivative products, as a reference rate for pricing valuation and cash flow determination. Therefore, LIBOR discontinuation will significantly impact companies’ arrangements in the Thai financial market and inter-company financing arrangements.

Therefore, companies in Thailand need to evaluate alternatives to their existing inter-company financing arrangements for a smoother transition into the post-LIBOR era.

A brief definition of some alternatives to LIBOR

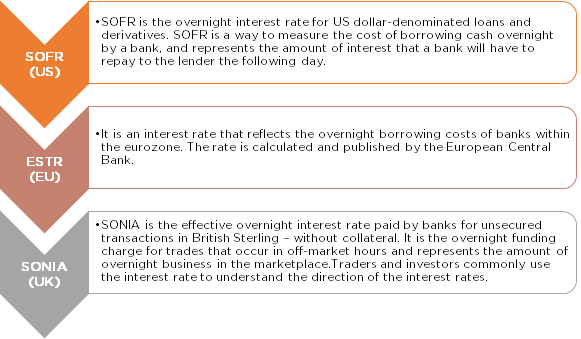

Some countries have already initiated the process of replacing LIBOR with alternate rates including, the secured overnight financing rate (SOFR) in the US, euro short-term rate (ESTR) in Europe, and sterling overnight interbank average rate (SONIA) in the UK.

TP implications on phasing out of LIBOR

As mentioned earlier, there is uncertainty about how multinational organizations will address the transition or how the arm’s length margin/spread will be calculated.

We set out below a few key considerations from a TP perspective that require immediate attention for a smoother transition into the post-LIBOR era.

Rearranging inter-company financing agreements

Intra-group financing transactions will be significantly affected, including loans and cash pooling arrangements, which referenced LIBOR as the base. In addition, LIBOR phase-out would require companies to either revise or cancel their existing intra-group financing agreements to reflect the conduct between the parties, as the agreements serve as the first line of defense during TP audits. Not updating or amending may expose multinationals to considerable risk for an adjustment from tax authorities.

Evaluate tax deductibility based on the selection of a potential option

Many companies follow centralized treasury operations to frame financing strategies, keeping tax planning and group synergies in focus. However, upon the transition, companies will need to evaluate the implications, including whether selecting one option increases the interest burden on the borrower or analyze the thin capitalization implications (where applicable), ensuring that the transition does not result in a restriction on tax deductibility. Presently, Thailand does not have thin capitalization rules.

Companies could also evaluate a decentralized approach, where subsidiaries could directly access funds from banks locally, wherever beneficial. This could assist groups in avoiding the administration of making or amending agreements on a year-on-year/periodic basis and avoiding inter-company transactions and the associated TP risks. However, a decentralized approach is only advisable on a case-by-case basis.

Risk mitigation/hedging strategies

Many companies operate cash pooling arrangements, and often, the cash pooler performs hedging activities. Therefore, the discontinuation of LIBOR is likely to create mismatches between the loan product and the related hedge, and that may lead to TP implications, which may require multinationals to restructure their cash pooling arrangements by determining the rates which the cash pooler should utilize in performing hedging activities efficiently. Therefore, multinationals need to initiate the analysis of an alternative interest rate mechanism pro-actively.

Availability and timing of the data

As businesses transition from LIBOR, which was easily assessable, the shifting to an alternative rate may initially pose challenges such as where to extract the data or understanding when and how often such data is published. Therefore, it is important to consider the availability and how swiftly the taxpayers and the tax authorities can assess the data for analysis.

Will your LIBOR analysis be of any use?

Due to the issues arising from the LIBOR transition, the TP documentation (from January 2022) prepared to support the LIBOR analysis may no longer be acceptable. Therefore, companies will need to re-strategies and undertake studies to support their prospective options for inter-company financing arrangements between the related parties pro-actively.

It will also be necessary to discuss the challenges and various options with regulators to make them on board in arriving or accepting one base rate to reduce future complications.

The Thai Revenue Department currently requires companies to submit details of their related parties and the transactions during the year if they report 200 million baht ($6.7 million) or more in revenues in an accounting period. Read more about online filing of Transfer Pricing disclosure forms.

Information related to loans is limited to the name of the related party, the amount of interest expense, interest income, and the balance of loans payable and receivable at the end of the accounting year. This information will be used to analyse and assess the next steps for determining the selection of taxpayers for TP audits. Read more about Transfer Pricing and tax audits in Thailand.

Assessing the impact of LIBOR phase-out for Thailand

The change will significantly impact financial arrangements from January 2022, and inter-company financing will not be excluded.

The Bank of Thailand (BOT), in collaboration with the Thai Bankers’ Association and the Association of International Banks, has established a Steering Committee on evaluating commercial banks’ preparedness on LIBOR discontinuation. The committee’s main objective is to ensure a smooth transition by focusing on the following areas:

- Amendment of financial contracts referencing LIBOR and THBFIX, including loans, notes, and derivative contracts;

- Preparation of commercial banks for LIBOR transition; and

- Development plan for alternative Thai reference rates.

The committee has recommended that market participants should assess outstanding contracts referencing LIBOR or THBFIX. Moreover, market participants should consult with commercial banks or counterparties in advance to amend existing contracts promptly. We also anticipate that the BOT would provide timely guidance to market participants and provide or suggest alternate rates to Thai companies such as in the US, Europe, and the UK.

Additionally, multinationals operating in Thailand or abroad generally make policies centrally, which the subsidiaries usually follow. As a result, the transition is likely to affect the tax structuring or planning of many multinationals. Multinationals will need to re-evaluate their inter-company financing arrangements to ensure that they are appropriate.

In addition, given the trend in cases selected for TP audits, many tax authorities worldwide are questioning multinational inter-company financing arrangements. Accordingly, the phase-out of LIBOR may serve as an opportunity for tax authorities, including the Thai Revenue Department, to target more inter-company financing transactions.

As the LIBOR phase-out will be effective by the end of 2021, we recommend that businesses operating in Thailand begin to evaluate the available alternatives and select the most appropriate and suitable option for their businesses (as highlighted above) or by initiating a dialog with the regulators to develop consistent policy.

Subsequently, the changes will need to be reflected in the inter-company agreements to move from LIBOR references to mitigate adverse tax or legal implications. In addition, it will be necessary for multinational groups to document such analysis appropriately in their TP documentation to support and document their TP policies.

Andrew Jackomos

Senior tax partner

E: andrew.j@hlbthailand.com

Rohit Sharma

Principal – transfer pricing

E: rohit.s@hlbthailand.com