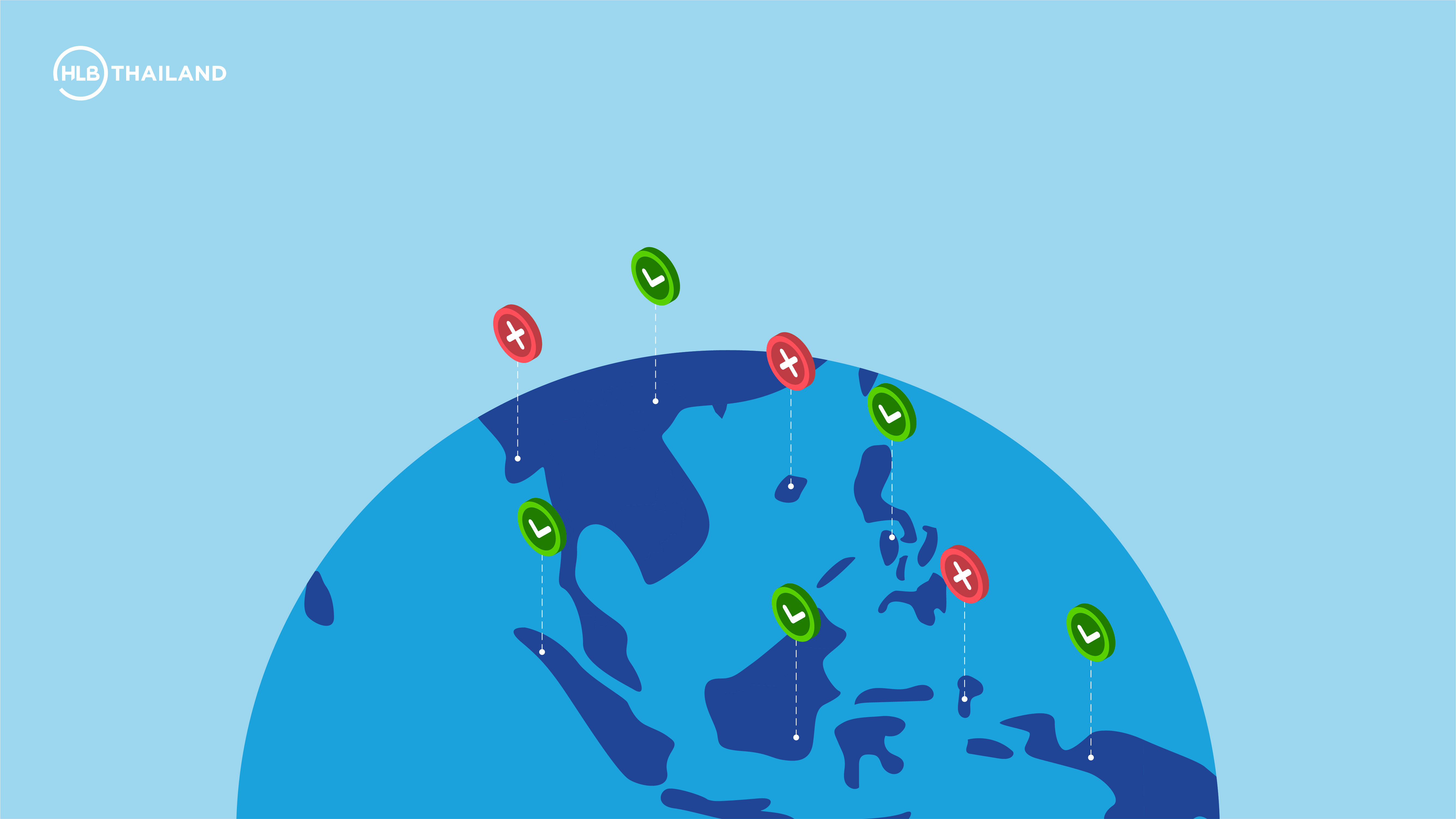

Which Southeast Asian Nations Have Adopted the OECD BEPS Action Plan 13?

HLB Thailand Transfer Pricing Team

The OECD first created the Base Erosion and Profit-Shifting (BEPS) action plan in 2016. Guidelines were initially adopted by 82 countries. Today, over 140 countries operate in line with the BEPS action plan.

Many countries within the ASEAN Economic Community (AEC) have since introduced their Country-by-Country report framework, as set out by the OECD. These include Country-by-Country Multilateral Competent Authority Agreements for the automatic exchange of information.

Here’s our breakdown of Transfer Pricing in Southeast Asia.

Read more: Everything you’ve ever wanted to know about Transfer Pricing in Thailand (with examples)

Vietnam

Vietnam’s economy is booming. Cheap labour costs are seeing the country become a popular manufacturing destination in Asia. To make sure all of this new business stays in check, the Ministry of Finance introduced its Transfer Pricing guidelines in 2017.

Transfer Pricing documentation should be maintained by Vietnamese companies with controlled transactions, to prove that pieces are at arm’s length.

But bear in mind, if your revenue is below VND 50bn (approx. USD 2.2m) and transactions with associated enterprises are below VND 30bn (approx. USD 1.3m), you don’t need to worry about preparing Transfer Pricing documentation in Vietnam.

Philippines

In recent years the Philippines has become an outsourcing hotspot, in part due to its substantial population of fluent English speakers. Naturally, the boom in multinational operations has raised widespread concerns about Transfer Pricing.

The chance of an annual tax audit in the Philippines is high, and there are no set penalties for Transfer Pricing issues. General tax penalties under the NIRC and other relevant laws will therefore apply. Because these fines will be based on percentages, they can be quite high.

Transfer Pricing documentation in the Philippines has become a requirement, and you’ll have to substantiate exactly how you’ve calculated the prices you charge for controlled transactions and calculate these prices as they happen, not at the end of the year.

You can find out more about the Philippines’ Transfer Pricing regulations here.

Malaysia

Malaysia joined many of its other Southeast Asian neighbours by implementing its Transfer Pricing guidelines in 2017. These are well-defined and extensive, following the OECD’s three-tiered approach. This requires the preparation of a local and master file, as well as country-by-country reporting along with the general Transfer Pricing documentation.

Cambodia

To combat perceived Transfer Pricing abuses and loss of tax revenue in Cambodia’s state budget, the Cambodian Ministry of Economy and Finance issued the Prakas 986 in 2017.

The Prakas 986 is based on the OECD’s Transfer Pricing Guidelines and requires the steps and results of the benchmarking process to be documented in an OECD-compliant TP document, preferably conforming to the guidance of the OECD’s BEPS Action 13 report of Country-by-Country reporting.

Indonesia

The Ministry of Finance in Indonesia unveiled regulation PMK 213 in December 2016, demanding a tighter deadline for compliance, and follows the guidance of the OECD’s BEPS Action 13.

Transfer Pricing documentation used to only be a requirement for a taxpayer’s operations in Indonesia. PMK-213 changed this. Now, taxpayers are required to follow the three-tiered structure, meaning a Master File, Local File and Country-by-Country Report will all be necessary.

Singapore

Singapore is an attractive option for businesses in Asia. To ensure this business is above board, the Ministry of Finance announced it will join the framework for the global implementation of the BEPS. This includes the requirement of Master File and Local File, as well as Country-by-Country reporting.

While taxpayers in Singapore aren’t required to submit Transfer Pricing documentation when filing tax returns, you’ll still need to provide everything within 30 days of receiving a request from the IRAS, so it’s best to keep everything on file.

Thailand

Thailand may have a reputation for being a bit slow off the mark when it comes to enforcing Transfer Pricing rules, but tighter regulation has finally arrived. There’s now a distinct need to get your Transfer Pricing documentation in order.

For the most part, Thailand’s Transfer Pricing regulations follow the OECD’s guidelines, with some distinct local details.

For example, Thailand’s new Transfer Pricing laws allow for 60 days to produce Transfer Pricing documentation once requested. If 60 days is too tight, you can request a further 60-day extension, and if it’s the first time the revenue department has requested Transfer Pricing documents from your company, a third 60 day extension is also possible. That gives first-timers a charitable 180 days to get their paperwork in order.

That said, Thailand’s tax authorities require local benchmarking for establishing whether your Transfer Pricing rates uphold the Arm’s Length Principle. That means you’ll need to keep a close eye on local market rates.

Additionally, the Thai tax authority’s statute of limitations extends for a full 5 years, requiring businesses to maintain extensive long term transaction records to avoid penalties and fees.

Read more: The impact of COVID-19 on your Transfer Pricing arrangements